Forget Finding the Needle, Leverage the Haystack & Reduce the Fees

Allocators search for hedge fund managers that they think will outperform their industry peers over time. Most allocators believe the best way to achieve their goal is by finding the best investment “talent” that will offer attractive future returns. Empirical evidence suggests it is very challenging to do so. Even for allocators with manager selection “edge”, the process of diligence and monitoring can be daunting. Then, when expectations are not met the agility to reposition away from a manager is often a slow cumbersome process.

At Unlimited, we believe there is an easier way to achieve differentiated outcomes than searching for the needle in the haystack. Modern replication approaches allow allocators to a) diversify the portfolio of managers without the burden and costs of additional diligence, b) reduce the fee drag and retain more of the return achieved. Investing in replication products that offer these advantages offers allocators the potential to overcome the outperformance odds.

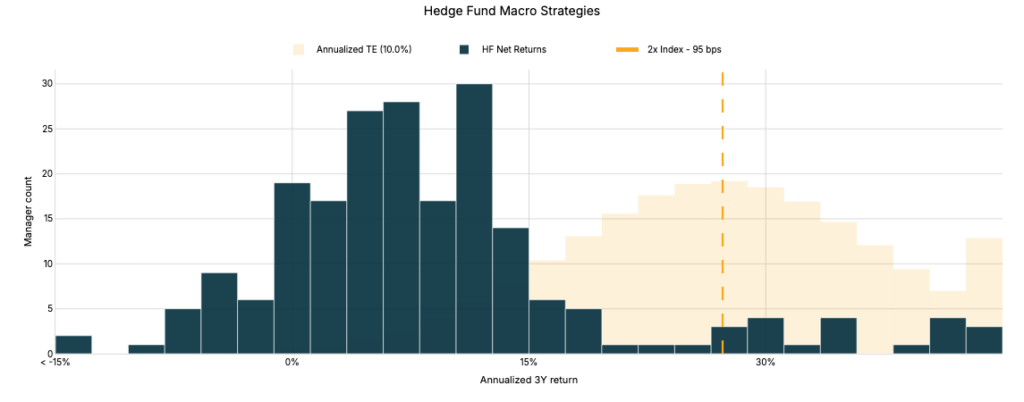

Global Macro managers serve as an illustrative example. The below chart depicts the return distribution of global macro hedge funds over the last three years. The gold shows what a replication approach running at 2x the target return with 95 bps of fees can offer, with the range estimating a 10% annualized tracking error. During this period the replication approach beats single manager selection in 88% of head-to-head selections.

Source: Unlimited Calculations, Preqin, Barclays, Pivotal Path, Bloomberg, HFR, EurekaHedge, Credit Suisse

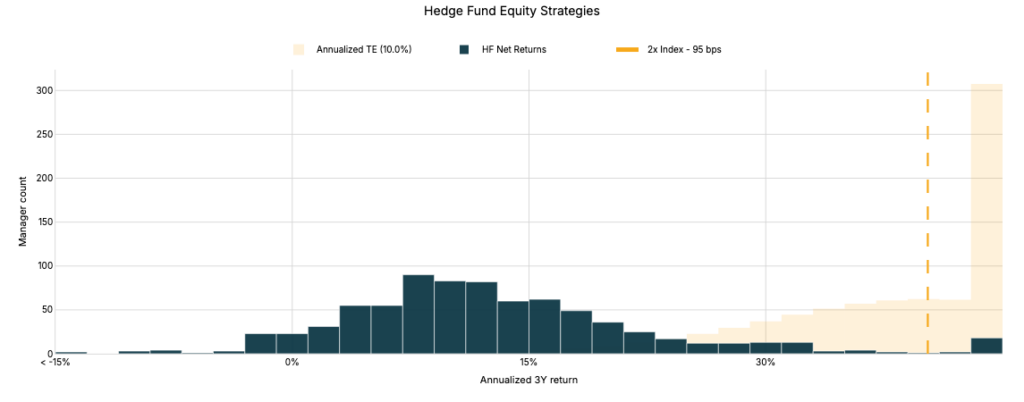

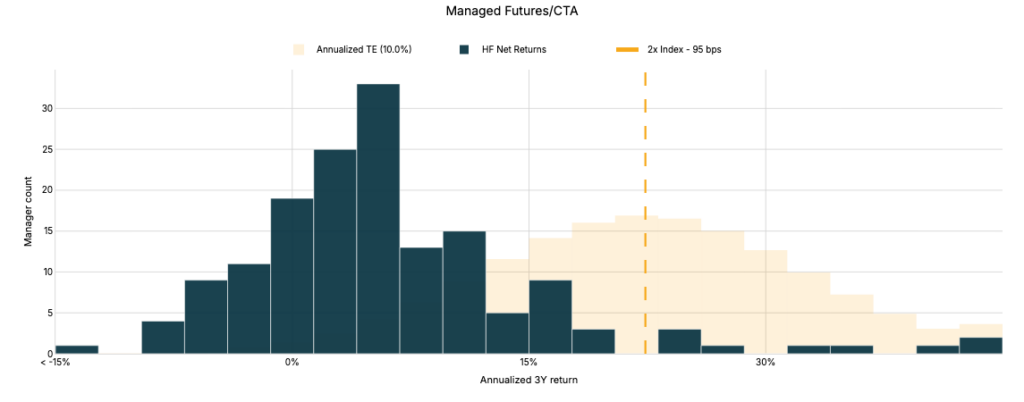

This trend is not limited to macro hedge funds. Data shows that long/short equity and managed futures hedge funds are also likely to underperform replication when run at a 2x target return with 95bps fees: 83% of the time for equity long/short and 92% of the time for managed futures.

Source: Unlimited Calculations, Preqin, Barclays, Pivotal Path, Bloomberg, HFR, EurekaHedge, Credit Suisse

Source: Unlimited Calculations, Preqin, Barclays, Pivotal Path, Bloomberg, HFR, EurekaHedge, Credit Suisse

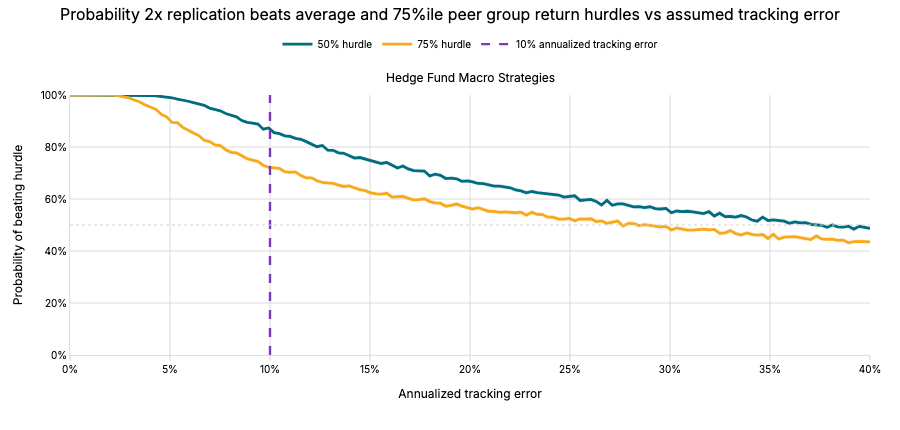

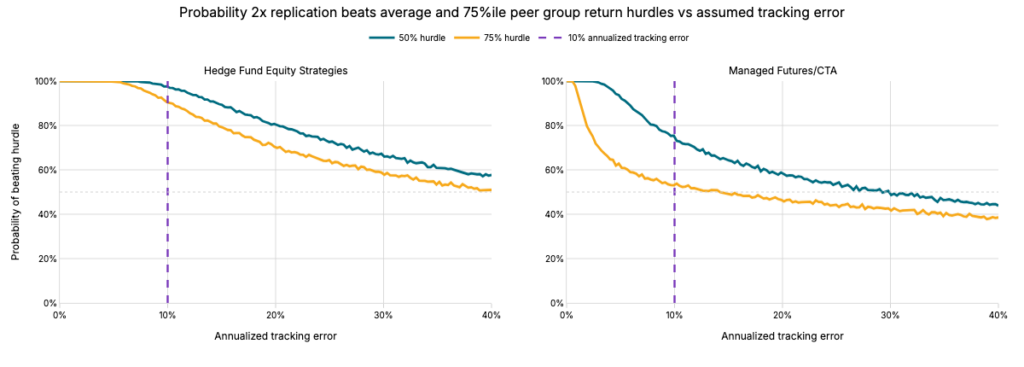

Some allocators are hesitant to eschew fund picking, often raising the concern of tracking error with replications since replicators don’t know the exact positions real time of all the managers in a cohort. However, the data shows that the replication doesn’t need to be anywhere near as honed as the above to have a solid chance of outperforming single manager selection.

The analysis below shows the probability of a global macro replication strategy outperforming single-manager selection as a function of the strategy’s tracking error. As long as the errors are consistent on both sides of the replication, upside errors can offset downside errors. Said another way, these strategies experience periods of outperforming the 2x index target and some of underperforming it, but the modeled data shows that the net impact results in an attractive result over time. Take global macro hedge funds as an example – even a replication with 20% error (2x what is shown above) outperforms single manager selection roughly two-thirds of the time.

Source: Unlimited Calculations, Preqin, Barclays, Pivotal Path, Bloomberg, HFR, EurekaHedge, Credit Suisse

The same pattern is largely true for equity long/short and managed futures hedge funds as well.

Source: Unlimited Calculations, Preqin, Barclays, Pivotal Path, Bloomberg, HFR, EurekaHedge, Credit Suisse

Allocators’ pursuit of a stellar single manager makes their job more difficult. Single-manager portfolios tend to be highly concentrated, and identifying true standouts is a challenge. Hedge fund replication may offer a simpler, more diversified alternative. By leveraging modern replication strategies, allocators have the opportunity to achieve equally competitive, top-quartile returns – even after accounting for tracking errors – without the burden of hunting for a needle in a haystack.

For informational and educational purposes only and should not be construed as investment advice. The historical analysis discussed herein has been selected solely to provide information on the development of the research and investment process and style of Unlimited. It does not constitute an offer to sell or a solicitation of an offer to buy any security. Opinions expressed are our present opinions only. No Representation is being made that any investment will or is likely to achieve profits or losses similar to those shown herein. Performance analysis herein is based on models and does not represent an investment outcome achieved by an actual investor. No representation is being made that any investor will or is likely to achieve results similar to those shown herein. No investment strategy or risk management technique can guarantee return or eliminate risk in any market environment. The material is based upon information which we consider reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. The historical analysis should not be construed as an indicator of the future performance of any investment vehicle that Unlimited manages.