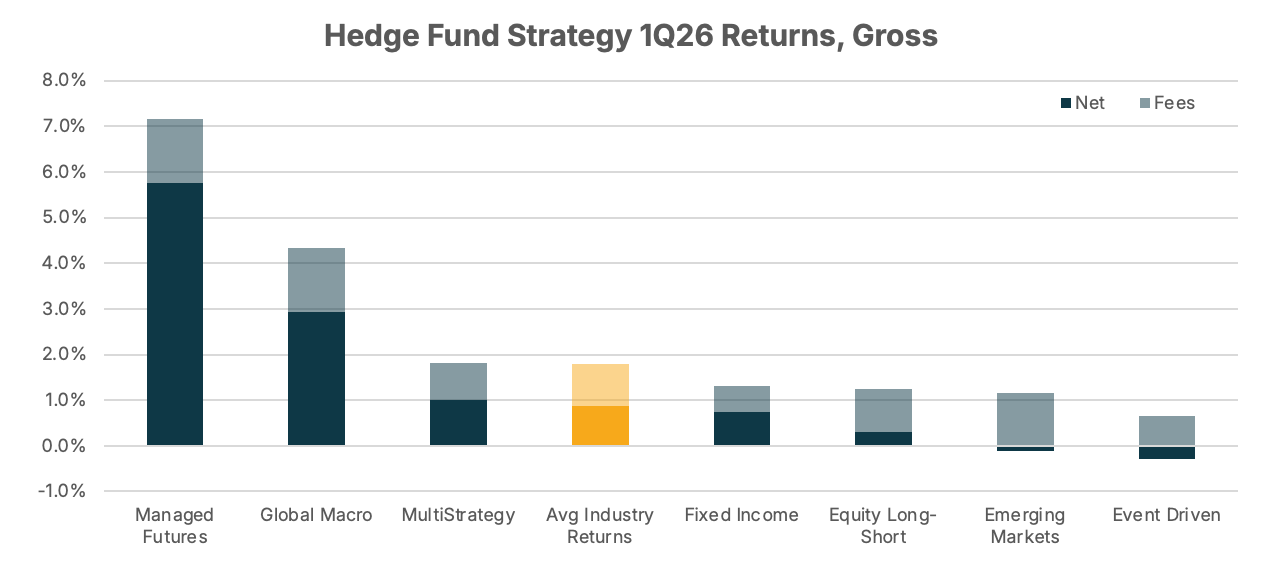

1Q 2026 Unlimited Hedge Fund Barometer

Hedge funds delivered positive performance in Q1 26 despite a major geopolitical shock, with Managed Futures and Global Macro strategies benefiting from rallies in gold and non-U.S. equities in the front-half of quarter. Event Driven strategies struggles amid a high-volatility environment.

Repeating Bogle’s Folly with Hedge Funds

Low cost index funds yield better returns than a portfolio of high cost managers. What was seen…

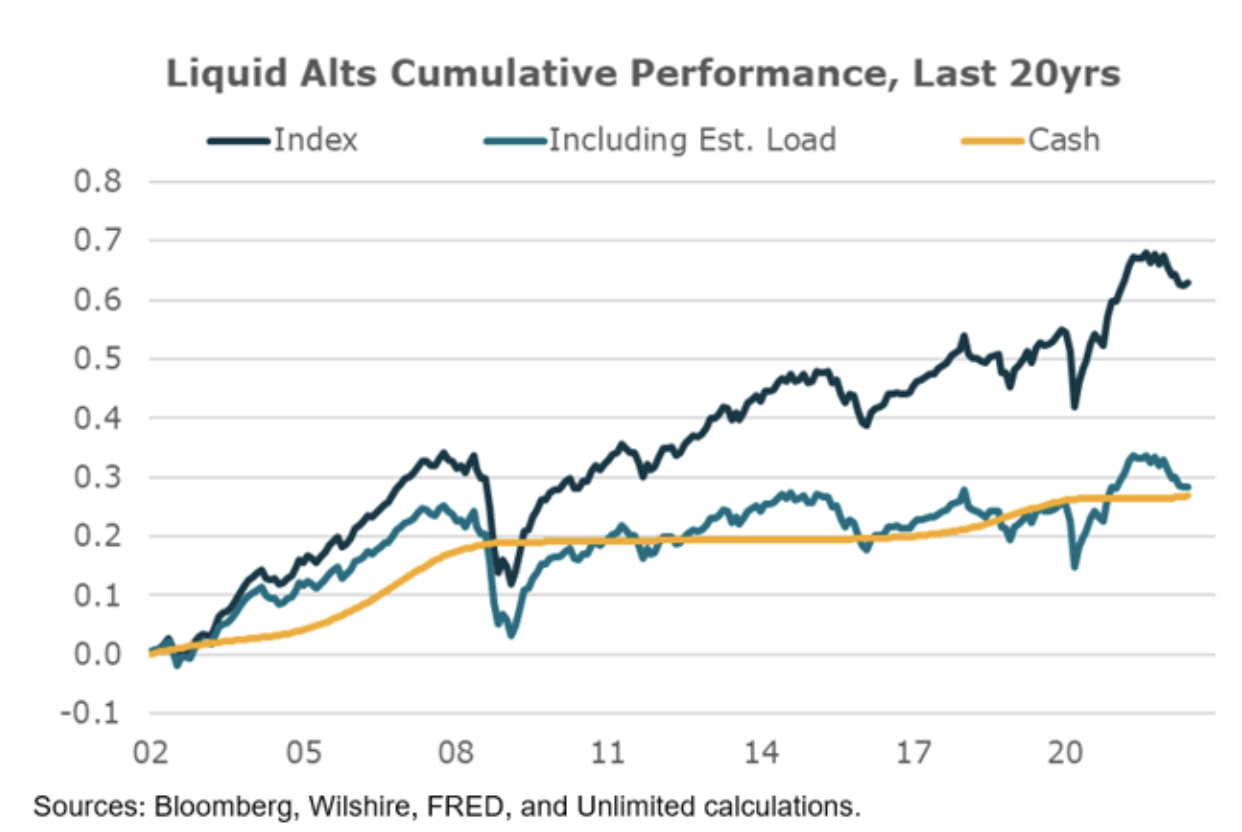

Today’s Liquid Alts Are a Terrible Deal For Investors

Managers of liquid alts have promised strong returns, low market correlation and better…