Published by Bob Elliott on Jun 21, 2022 3:24:33 PM

Global Macro funds are having one of their best years ever. Retail investors are having one of their worst in some time. The divergence in positioning between these two sets of investors is the starkest in history. When these divergences have occurred in the past, Global Macro managers have made money and retail investors haven’t – suggesting that Macro managers are the ‘smart money.’

While most investors can’t invest directly into Global Macro funds, our return replication technology allows us to infer hedge fund managers positioning in real time. From what we see, a shift toward global macro manager positioning requires adding commodity and gold positions and cutting back on stock and bond leverage even taking into consideration the moves so far.

The chart below highlights the divergence in returns between Unlimited’s Global Macro replication and the returns of a typical US retail investor (75/25 stocks bonds). So far this year there has been a divergence of nearly 40%.

The returns shown are for illustrative purposes only and do not represent the composition of any portfolio or account managed by Unlimited and available for investment by others. Simulated, backtested, modeled, or hypothetical performance results have certain inherent limitations and are for illustrative purposes only. Such results are hypothetical and do not represent actual trading, and thus may not reflect material economic and market factors, such as liquidity constraints, that may have had an impact on actual decision-making. Such results are also achieved through retroactive application of a model designed with the benefit of hindsight and cannot account for all financial risk that may affect actual performance. No representation is being made that any investor will or is likely to achieve results similar to those shown.

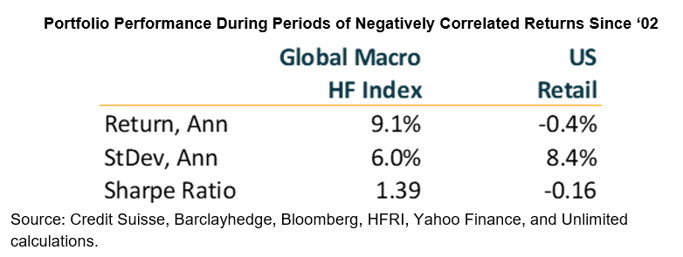

This is the biggest divergence in performance in decades. The rolling 12m correlation of our composite Global Macro index to 75/25 stocks/bonds has been -80%.

When there is a divergence between the two, Global Macro managers are the ‘smart money.’ Below we take all the periods where there is negative correlation between the returns of Global Macro managers and retail performance. When views diverge, Global Macro managers make money and retail doesn’t.

We infer the positioning of Global Macro managers using our technology and today we see these funds are holding positions that are significantly different from retail investors. The chart below shows the positioning of Global Macro managers across major asset classes (there are diff in these asset classes that our technology picks up, but we have simplified it to asset class level for ease of understanding and since it covers the majority of the risk). Global Macro managers are long commodities and gold, neither of which are in most retail portfolios. These managers are also short bonds and close to neutral on stocks.

During volatile market environments, it’s critical for investors to find the ‘smart money’ positions that are well suited to the market environment. Global Macro managers have shown their ability to outperform in these environments, and Unlimited’s return replication technology can see in real time how managers are positioned. Even if these funds aren’t investible, the information can be leveraged by investors to better position themselves by following this ‘smart money.’